From churches to youth organizations to the local chambers of commerce, nonprofit organizations make our communities more livable places. Unlike for-profit businesses that exist to generate profits for their owners, nonprofit organizations exist to pursue missions that address the needs of society. Nonprofit organizations serve in a variety of sectors, such as religious, education, health, social services, commerce, amateur sports clubs, and the arts.

Illustration of the Statement of Financial Position and the Statement of Activities

We are now ready to present examples of the statement of financial position and the statement of activities. To do that, we'll follow the activities of a nonprofit organization called Home4U, a daytime shelter for adults.

Let's assume that Home4U was incorporated in January 2013 and its accounting years will end on each December 31. The following transactions occurred during a three-month period.

Statement of Functional Expenses

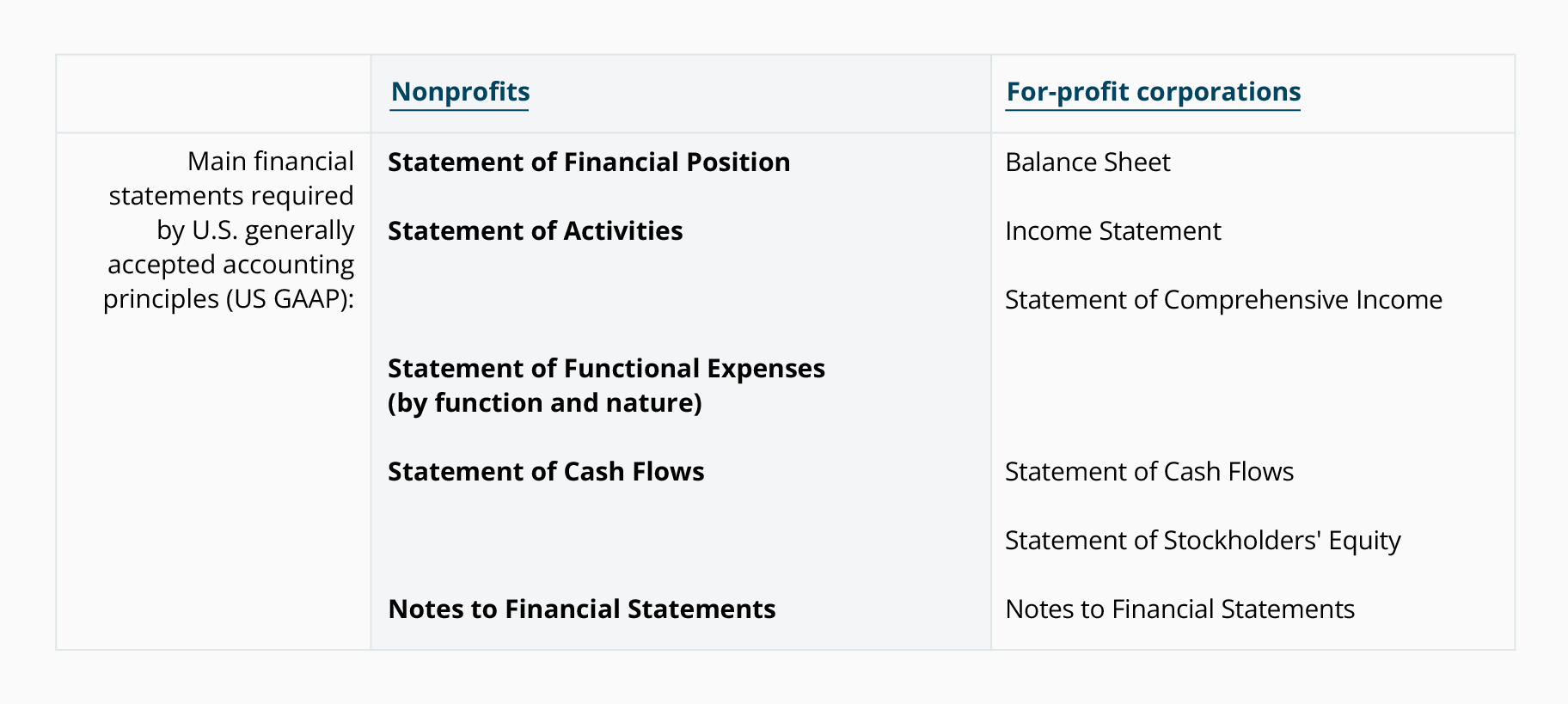

The statement of functional expenses is described as a matrix since it reports expenses by their function (programs, management and general, fundraising) and by the nature or type of expense (salaries, rent). For instructional purposes we highlighted the column headings to indicate the expenses by function. We also highlighted the words in the first column as they indicate the nature or type of expenses.

Introduction to Payroll Accounting

It's a fact of business—if a company has employees, it has to account for payroll and fringe benefits.

In this explanation of payroll accounting we'll introduce payroll, fringe benefits, and the payroll-related accounts that a typical company will report on its income statement and balance sheet. Payroll and benefits include items such as:

Salaries, Wages, & Overtime Pay

In this section of payroll accounting we focus on the gross amounts earned by the employees of a company.

Salaries

Salaries are usually associated with "white-collar" workers such as office employees, managers, professionals, and executives. Salaried employees are often paid semi-monthly (e.g., on the 15th and last day of the month) or bi-weekly (e.g., every other Friday) and their salaries are often stated as a gross annual amount, such as "$48,000 per year." The "gross" amount refers to the pay an employee would receive before withholdings are made for such things as taxes, contributions to United Way, and savings plans.

Payroll Withholdings: Taxes & Benefits Paid by Employees

This section of payroll accounting focuses on the amounts withheld from employees' gross pay. (In Part 4 of payroll accounting we will discuss the payroll taxes that are not withheld from employees' gross pay.)

Payroll Taxes, Costs & Benefits Paid by Employers

In addition to salaries and wages, the employer will incur some or all of the following payroll-related expenses:

- Employer portion of Social Security tax

- Employer portion of Medicare tax

- State unemployment tax

- Federal unemployment tax

- Worker compensation insurance

- Employer portion of insurance (health, dental, vision, life, disability)

- Employer paid holidays, vacations, and sick days

- Employer contributions toward 401(k), savings plans, & profit-sharing plans

- Employer contributions to pension plans

- Post-retirement health insurance

Examples of Payroll Journal Entries For Wages

NOTE: In the following examples we assume that the employee's tax rate for Social Security is 6.2% and that the employer's tax rate is 6.2%. (During the years 2011 and 2012 only, the employee's rate was reduced to 4.2%.)

In this section of payroll accounting we will provide examples of the journal entries for recording the gross amount of wages, payroll withholdings, and employer costs related to payroll.

Examples of Payroll Journal Entries For Salaries

Note: In the following examples we assume that the employee's tax rate for Social Security is 6.2% and that the employer's tax rate is 6.2%. (During 2011 and 2012 only, the employee's rate was reduced to 4.2%.)

Let's assume our company also has salaried employees who are paid semimonthly on the 15th and the last day of each month. The pay period for these employees is the half-month that ends on payday. There is one salaried employee in the warehouse department with a gross salary of $48,000 per year, or $2,000 per pay period. There are four salaried employees in the Selling & Administrative Department with combined salaries of $9,000 per pay period.

Introduction to Bookkeeping

The term bookkeeping means different things to different people:

- Some people think that bookkeeping is the same as accounting. They assume that keeping a company's books and preparing its financial statements and tax reports are all part of bookkeeping. Accountants do not share their view.

Accrual Method

There are two main methods of accounting (or bookkeeping):

- Accrual method

- Cash method

The accrual method of accounting is the preferred method because it provides:

Double-Entry, Debits and Credits

Double-Entry

Except for some very small companies, the standard method for recording transactions is double-entry. Double-entry bookkeeping or double-entry accounting means that every transaction will involve at least two accounts. To illustrate, here are a few transactions and the two accounts that will be affected:

General Ledger Accounts

The accounts that are used to sort and store transactions are found in the company's general ledger. The general ledger is often arranged according to the following seven classifications. (A few examples of the related account titles are shown in parentheses.)

Debits and Credits in the Accounts

If you already understand debits and credits, the following table summarizes how debits and credits are used in the accounts.

Subscribe to:

Comments (Atom)