The balance sheet is one of the four main financial statements of a business:

The balance sheet reports a company's assets, liabilities, and stockholders' equity as of a moment in time. (The other three financial statements report amounts for a period of time such as a year, quarter, month, etc.) The balance sheet is also known as the statement of financial position and it reflects the accounting equation:

Assets = Liabilities + Stockholders' Equity.

Bankers will look at the balance sheet to determine the amount of a company's working capital, which is the amount of current assets minus the amount of current liabilities. They will also review the assets and the liabilities and compare these amounts to the amount of stockholders' equity.

When a balance sheet reports at least one additional column of amounts from an earlier balance sheet date, it is referred to as a comparative balance sheet.

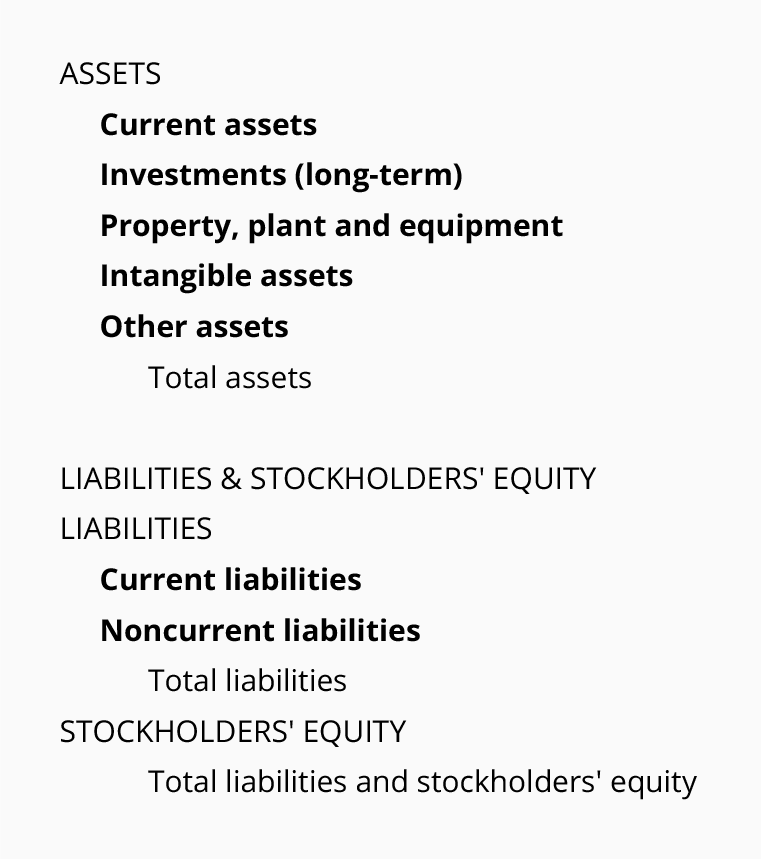

Balance Sheet Classifications

Typically, companies issue a classified balance sheet. This means that the amounts are presented according to the following classifications:

Descriptions of the balance sheet classifications

The following are brief descriptions of the classifications usually found on a company's balance sheet.

Current assets

Generally, current assets include cash and other assets that are expected to turn to cash within one year of the date of the balance sheet. Examples of current assets are cash and cash equivalents, short-term investments, accounts receivable, inventory and prepaid expenses.

Generally, current assets include cash and other assets that are expected to turn to cash within one year of the date of the balance sheet. Examples of current assets are cash and cash equivalents, short-term investments, accounts receivable, inventory and prepaid expenses.

Investments

This classification is the first of the noncurrent or long-term assets. Included are long-term investments in other companies, the cash surrender value of life insurance, bond sinking funds, real estate held for sale, and cash that is restricted for construction of plant and equipment.

This classification is the first of the noncurrent or long-term assets. Included are long-term investments in other companies, the cash surrender value of life insurance, bond sinking funds, real estate held for sale, and cash that is restricted for construction of plant and equipment.

Property, plant and equipment

This category of noncurrent assets includes the cost of land, buildings, machinery, equipment, furniture, fixtures, and vehicles used in the operations of a business. Except for land, these assets will be depreciated over their useful lives.

This category of noncurrent assets includes the cost of land, buildings, machinery, equipment, furniture, fixtures, and vehicles used in the operations of a business. Except for land, these assets will be depreciated over their useful lives.

Intangible assets

Intangible assets include goodwill, trademarks, patents, copyrights and other non-physical assets that were acquired at a cost. The amount reported is their cost to acquire minus any amortization or write-down due to impairment. Valuable trademarks and logos that were developed by a company through years of advertising are not reported because they were not purchased from another person or company.

Intangible assets include goodwill, trademarks, patents, copyrights and other non-physical assets that were acquired at a cost. The amount reported is their cost to acquire minus any amortization or write-down due to impairment. Valuable trademarks and logos that were developed by a company through years of advertising are not reported because they were not purchased from another person or company.

Other assets

This category often includes costs that have been paid but are being expensed over a period greater than one year. Examples include bond issue costs and certain deferred income taxes.

This category often includes costs that have been paid but are being expensed over a period greater than one year. Examples include bond issue costs and certain deferred income taxes.

Current liabilities

Current liabilities are obligations of a company that are payable within one year of the date of the balance sheet (and will require the use of a current asset or will be replaced with another current liability).

Current liabilities are obligations of a company that are payable within one year of the date of the balance sheet (and will require the use of a current asset or will be replaced with another current liability).

Current liabilities include loans payable that will be due within one year of the balance sheet date, the current portion of long-term debt, accounts payable, income taxes payable and liabilities for accrued expenses.

Noncurrent liabilities

These are also referred to as long-term liabilities. In other words, these obligations will not be due within one year of the balance sheet date. Examples include portions of automobile loans, portions of mortgage loans, bonds payable, and deferred income taxes.

These are also referred to as long-term liabilities. In other words, these obligations will not be due within one year of the balance sheet date. Examples include portions of automobile loans, portions of mortgage loans, bonds payable, and deferred income taxes.

Stockholders' equity

This section of the balance sheet consists of the following major sections:

This section of the balance sheet consists of the following major sections:

- Paid-in capital (the amounts paid by investors when the original shares of a corporation were issued)

- Retained earnings (the earnings of the corporation since it began minus the amounts that were distributed in the form of dividends to the stockholders)

- Treasury stock (a subtraction that represents the amount paid to repurchase the corporation's own stock)

Additional information on the balance sheet

To learn more about the balance sheet use any of the following links:

Income Statement

The income statement is also known as the statement of operations, the profit and loss statement, or P&L. It presents a company's revenues, expenses, gains, losses and net income for a specified period of time such as a year, quarter, month, 13 weeks, etc.

Income Statement Formats

There are two formats for presenting a company's income statement:

- Multiple-step

- Single-step

The difference in formats has to do with the number of subtractions and subtotals that appear on the income statement before getting to the company's bottom line net income.

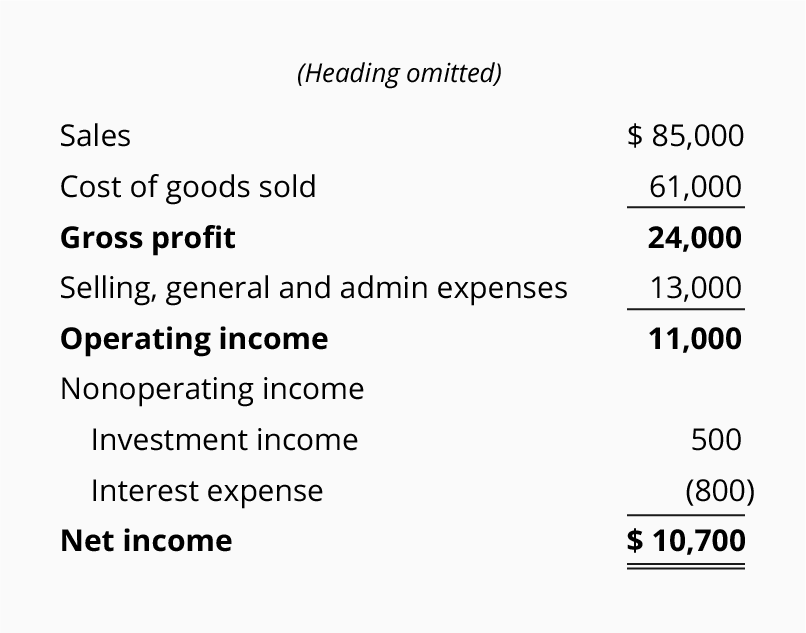

Multiple-step income statement

Note that in the following multi-step income statement, there are three subtractions:

Note that in the following multi-step income statement, there are three subtractions:

- The first subtraction results in the subtotal gross profit.

- The second subtraction results in the subtotal operating income.

- The third subtraction provides the bottom line net income.

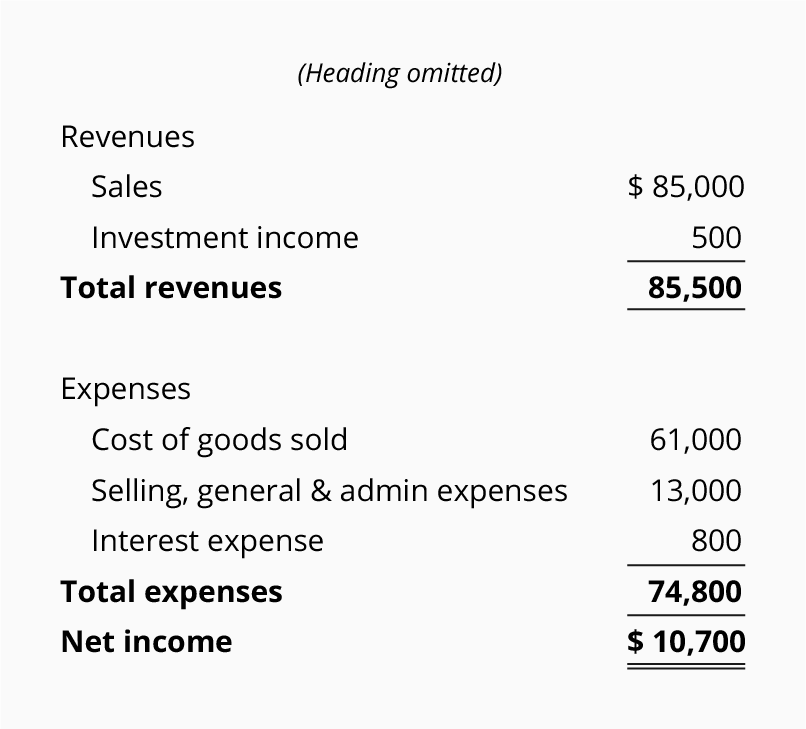

Single-step income statement

In the single-step format, the income statement will have only one subtraction—all of the expenses (both operating and non-operating) are subtracted from all of the revenues (both operating and non-operating). In this format, there is no subtotal for gross profit or operating income. The bottom line, net income, results from a single subtraction (a single step) as shown here:

In the single-step format, the income statement will have only one subtraction—all of the expenses (both operating and non-operating) are subtracted from all of the revenues (both operating and non-operating). In this format, there is no subtotal for gross profit or operating income. The bottom line, net income, results from a single subtraction (a single step) as shown here:

Balance Sheet and Income Statement are Linked

As we had discussed earlier, revenues cause stockholders' equity to increase while expenses cause stockholders' equity to decrease. Therefore, a positive net income reported on the income statement (which is the result of revenues being greater than expenses) will cause stockholders' equity to increase. A negative net income will cause stockholders' equity to decrease.

The income statement accounts are temporary accounts because their balances will be closed at the end of each accounting year to the stockholders' equity account Retained Earnings. (The balances in a sole proprietorship's income statement accounts will be closed to the owner's capital account.)

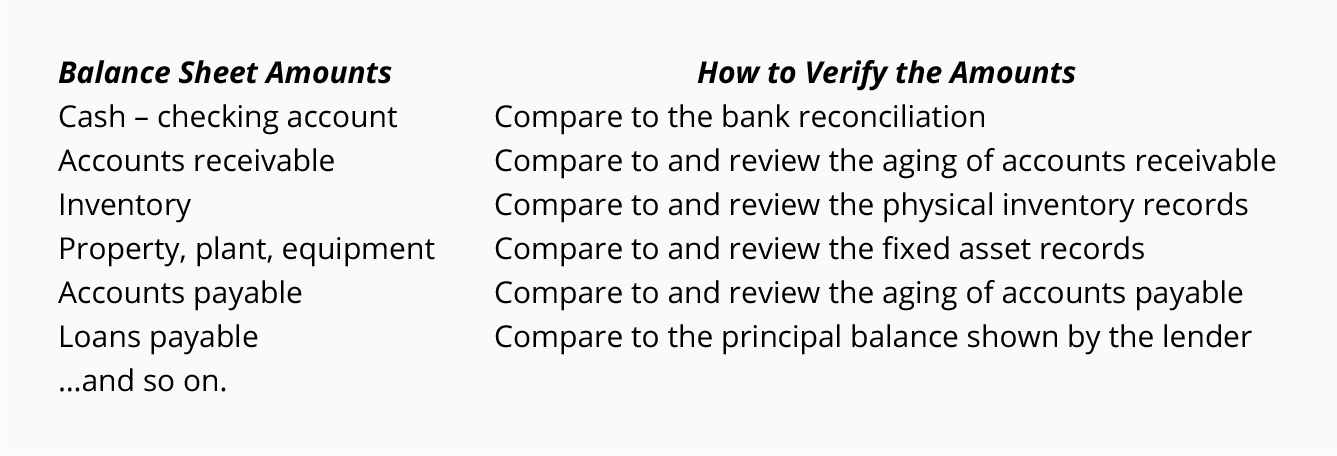

The link between the balance sheet and income statement is helpful for bookkeepers and accountants who want some assurance that the amount of net income appearing on the income statement is correct. If you verify the ending balances in the relatively few balance sheet accounts, you can have confidence that the income statement has the proper net income. Hence, you are wise to establish a routine to verify all of the balance sheet amounts.

Note: This technique does not guarantee that the details within the income statement are perfect.

Here is our suggestion for reviewing the balance sheet amounts.

Additional review

Another review that should be done routinely is to compare each item on the income statement to the same item on an earlier income statement. For example, the amounts for the 5-month period of the current year should be compared to the 5-month period of the previous year. If budgets are prepared, also compare this year's 5-month period to the budgeted amounts for the 5-month period.

The same holds for the balance sheet: compare the recent amounts to the amounts on the balance sheets from a year earlier and from a month earlier.

No comments:

Post a Comment