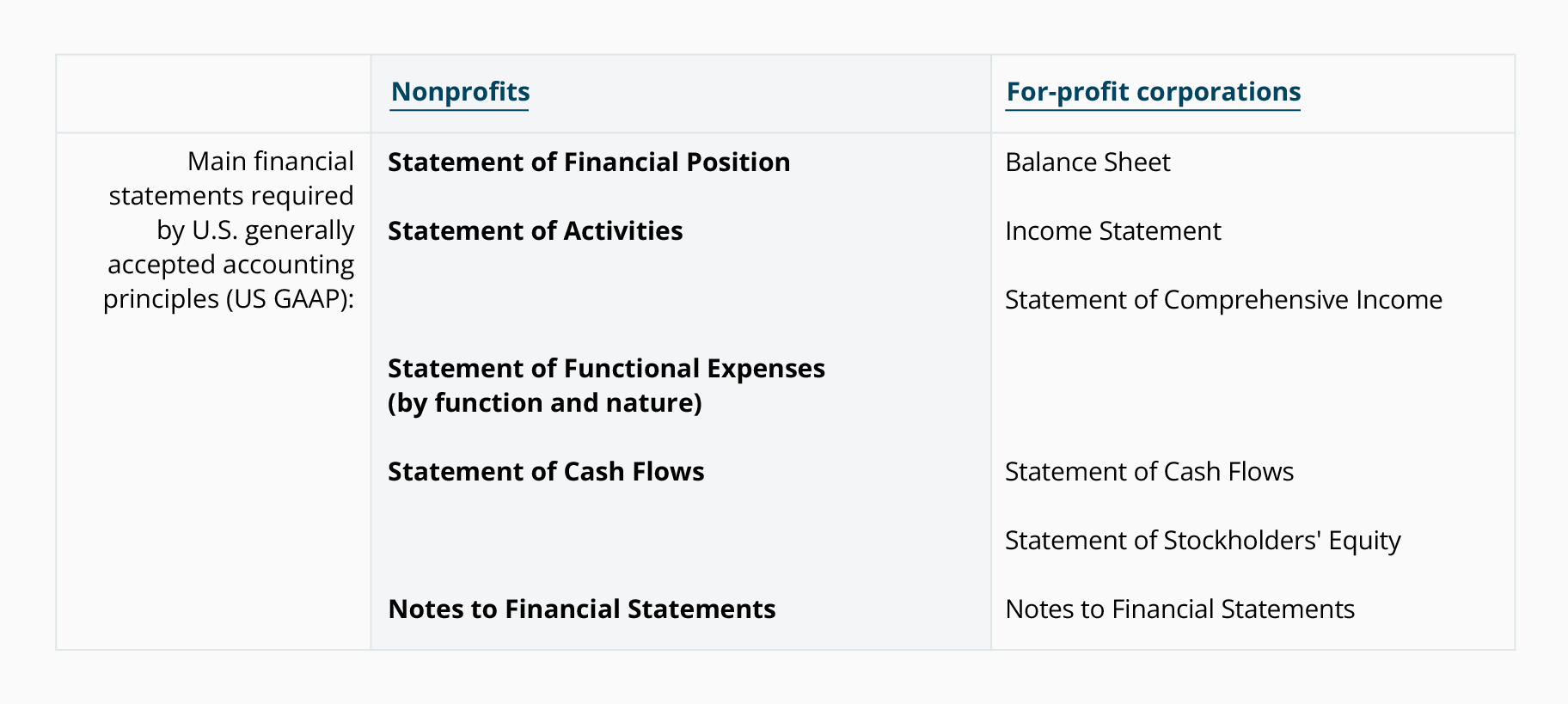

The following table compares the main financial statements of a nonprofit organization with those of a for-profitcorporation.

Statement of Financial Position

A nonprofit's statement of financial position (similar to a business's balance sheet) reports the organization's assets and liabilities in some order of when the assets will turn to cash and when the liabilities need to be paid. The amounts are as of the date shown in the heading which is usually the end of a month, quarter, or year. (We will present a sample statement of financial position in a later section.)

Net Assets

Since a nonprofit organization does not have owners, the third section of the statement of financial position is known as net assets (instead of owner's equity or stockholders' equity).

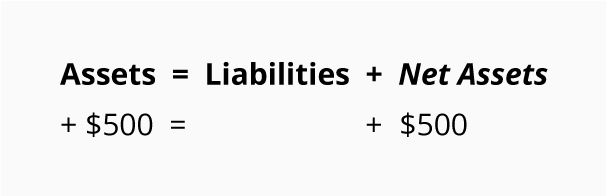

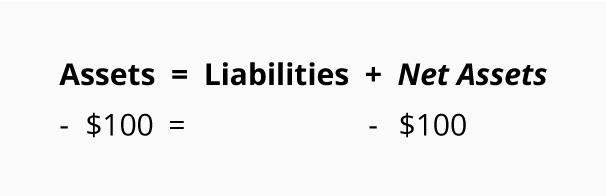

A nonprofit's statement of financial position is represented by the following accounting equation:

Because of double-entry bookkeeping, the accounting equation and the statement of financial position should remain in balance at all times. For example, if a donor contributes $500, the effect on the nonprofit's accounting equation and its statement of financial position is:

If the nonprofit pays $100 for supplies that will be used immediately, the effect on its accounting equation and its statement of financial position is:

The items that cause the changes in Net Assets are reported on the nonprofit's statement of activities (to be discussed later).

The net assets section of a nonprofit's statement of financial position reports totals for each of the following classifications:

- Unrestricted net assets

- Temporarily restricted net assets

- Permanently restricted net assets

These classifications are based on the restrictions made by the donors at the time of their contributions.

1. Unrestricted net assets

If a donor does not specify a restriction on his or her contribution, the amount received by the nonprofit is recorded as an asset and as unrestricted contribution revenues. Unrestricted contribution revenues (reported on the statement of activities) also cause the amount of unrestricted net assets to increase. For instance, if a nonprofit receives an unrestricted contribution of $800 of cash, the effect on the statement of financial position is:

If the nonprofit's board of directors designates some of the nonprofit's unrestricted assets for a specific purpose, those assets must continue to be reported as unrestricted net assets.

2. Temporarily restricted net assets

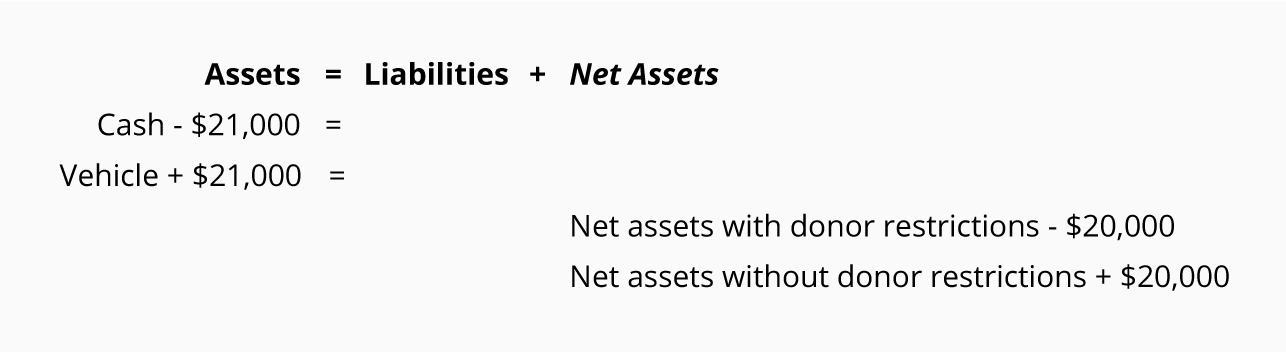

If a nonprofit receives a contribution that has a donor-imposed restriction (other than to be held in perpetuity), the amount is usually recorded as an asset and as temporarily restricted contribution revenues. Temporarily restricted contribution revenues (reported on the statement of activities) also cause the amount of temporarily restricted net assets to increase. For example, James donates $20,000 with the requirement that the nonprofit use it to purchase a vehicle that is urgently needed in one of the nonprofit's programs. The effect on the nonprofit's accounting equation at the time the contribution is received is:

When the nonprofit purchases the vehicle at a cost of say $21,000, the purchase and the release of the restriction will cause the following changes:

To gain a further understanding of temporary restrictions, you should read the FASB's standards cited in the final section of our discussion, Sources for More Information of Nonprofit Accounting.

3. Permanently restricted net assets

If a donor stipulates that her contribution must be held by the nonprofit in perpetuity (forever, not be used up), the amount is recorded as an asset and as permanently restricted contribution revenues. Permanently restricted contribution revenues (reported on the statement of activities) also cause the amount of permanently restricted net assets to increase. To illustrate, let's assume that Mary contributes $100,000 to a nonprofit and stipulates that only the interest on the $100,000 can be spent. This contribution will have the following affect on the nonprofit's statement of financial position:

If Mary also stipulates that the interest earned must be used for scholarships and $3,000 is earned on the $100,000, the $3,000 must be reported as temporarily restricted net assets until the restriction is released by the payment for scholarships.

Total net assets

The grand total of the three classifications of net assets is reported as Net Assets or as Total Net Assets.

Statement of Activities

Since a nonprofit's primary purpose is to provide programs that meet certain societal needs, it issues a statement of activities (instead of the income statement that is issued by a for-profit business).

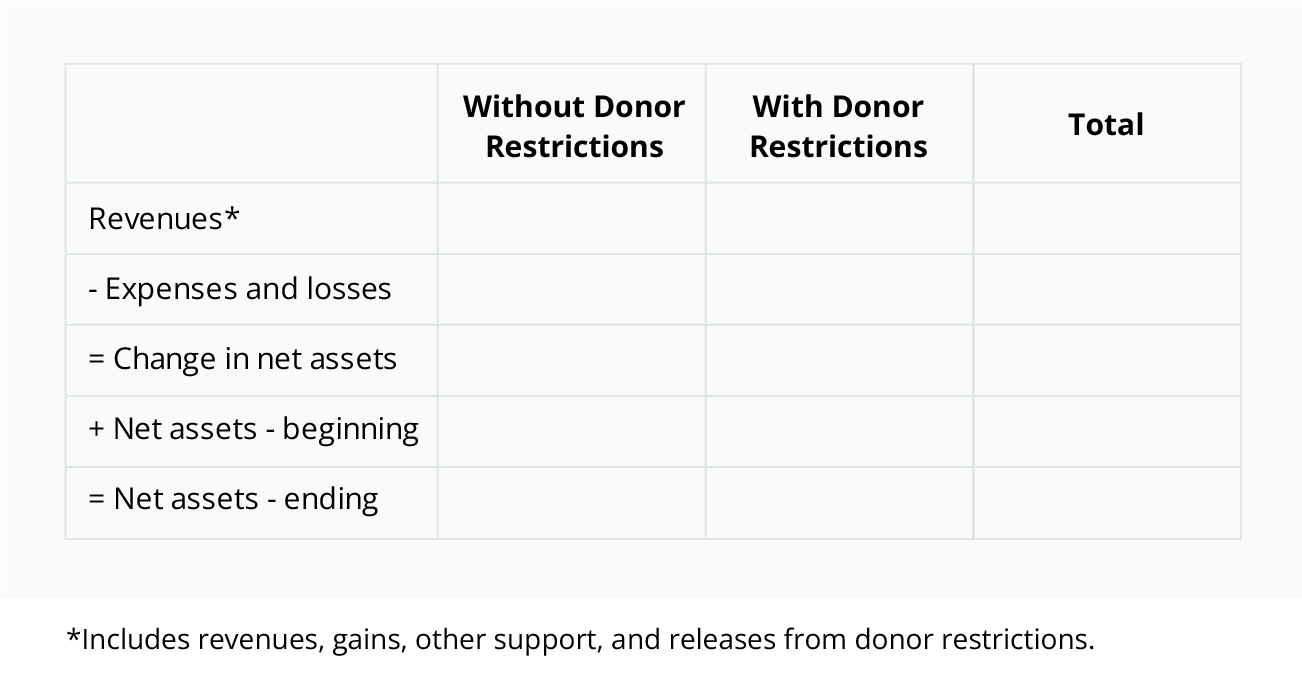

The statement of activities reports revenue and expense amounts according to the three classifications of net assets discussed above. Here is an outline of the statement of activities without its heading and without amounts:

* Revenues often include the reclassification of net assets at the time they are released from restriction.

Before we illustrate a sample statement of activities, let's take a closer look at its components.

Revenues and Expenses

During any given accounting period, Revenues and Expenses are the two primary sections where summarized transaction amounts will be reported.

Revenues

The caption Revenues is often expanded to be more descriptive. Here are some of the possibilities:

- Support and Revenues

- Revenues, Support and Reclassifications

- Revenues, Gains and Other Support

- some variation of the above or a more descriptive caption

Revenues that may be listed on the statement of activities include:

- Contributions

- Membership dues

- Program fees

- Fundraising events

- Grants

- Investment income

- Gain on sale of investments

- Reclassifications when net assets are released from restrictions (a negative amount in the temporarily restricted column and a positive amount in the unrestricted column)

Under the accrual method of accounting, revenues are reported in the accounting period in which they are earned. In other words, revenues might be earned in an accounting period that is different from the period in which the cash is received.

Expenses

The caption Expenses could be termed Functional Expenses since expenses are reported according to these functions:

- Program expenses

- Supporting services expenses

1. Program expenses

Program expenses (or program services expenses) are the amounts directly incurred by the nonprofit in carrying out its programs. For instance, if a nonprofit has three main programs, then each of the three programs will be listed along with each program's expenses.

2. Supporting services expenses

Supporting services expenses are reported in two subgroups:

- Management and general

- Fundraising

In order to accurately report the amount in each of these subgroups, it may be necessary to allocate some management and general salaries to fundraising based on the time spent by employees performing fundraising activities. For example, a management employee might be spending 30% of her time in fundraising activities but her entire salary has been recorded as management and general expenses.

Under the accrual method of accounting, expenses are to be reported in the accounting period in which they best match the related revenues. If that is not clear, then the expenses should be reported in the period in which they are used up. If there is uncertainty as to when an expense is matched or is used up, the amount spent should be reported as an expense in the current period.

General Ledger Accounts and Chart of Accounts

A nonprofit's transactions are recorded in accounts in the general ledger. A listing of the titles of the general ledger accounts is known as the chart of accounts.

The accounts in the general ledger and in the chart of accounts are organized as follows:

- statement of financial position accounts

- asset accounts

- liability accounts

- net asset accounts

- statement of activities accounts

- revenues and gains

- expenses and losses

To view some of the account titles that may appear in the above categories see our Detailed Chart of Accounts.

The number of accounts in a nonprofit's general ledger could range from 30 to 1,000 or more. The number of accounts depends on the number of programs that the nonprofit has, the types of revenues it earns, and the level of detail required for planning and control of the organization.

For example, a nonprofit is likely to have a separate general ledger account for each of its bank accounts. It may also have 50 general ledger accounts for each of its major programs, plus many accounts under its fundraising and management and general expense categories.

The detail in the general ledger accounts will always be available for management's use. However, all of the account balances will be summarized into a few totals that are presented in the financial statements and IRS Form 990.

Nonprofit recordkeeping can get a bit challenging, so it is worth noting that accounting software exists to help nonprofits record transactions efficiently. The accounting software will also allow for reports of revenues and expenses by function (programs, fundraising, management and general), by the nature or type of expense (salaries, electricity, rent, depreciation, etc.), and/or by grant.

No comments:

Post a Comment