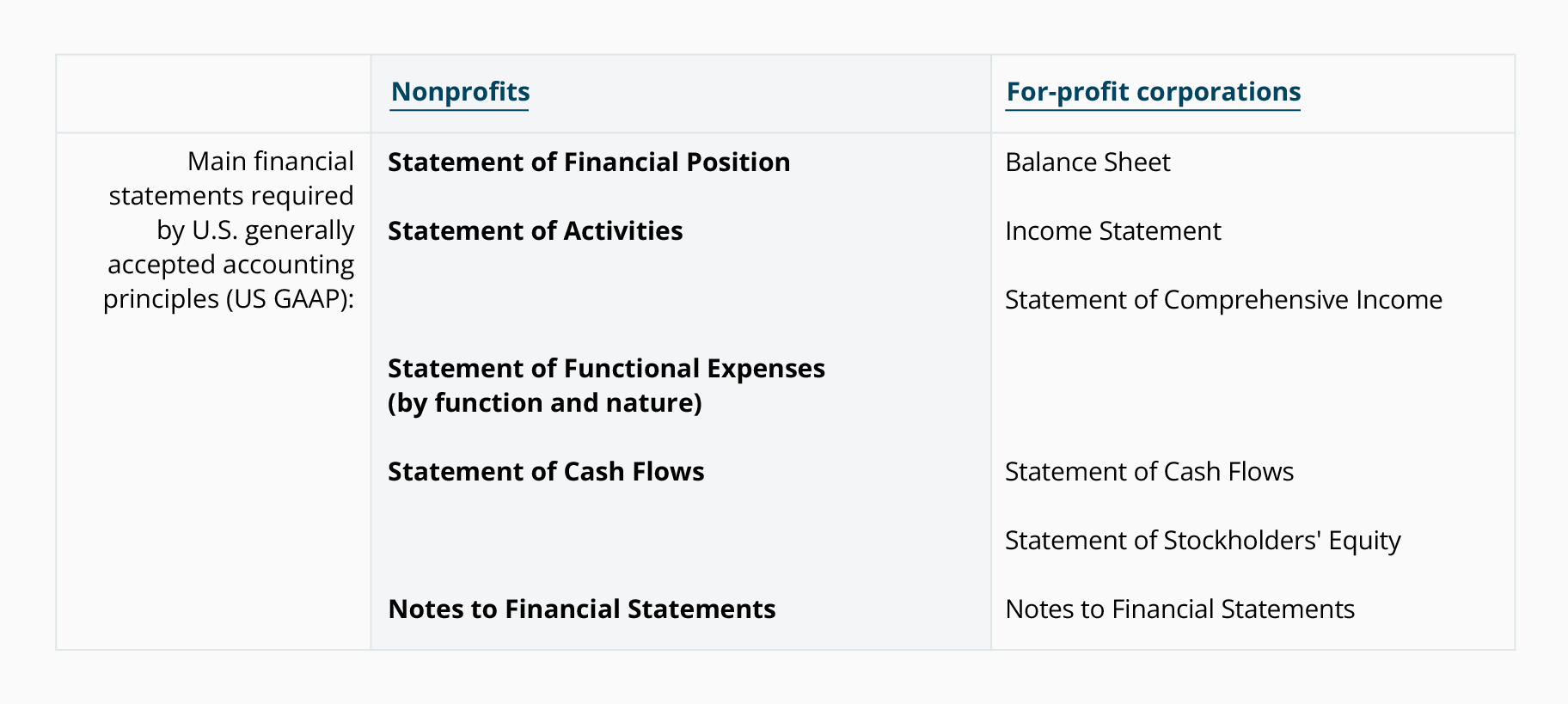

From churches to youth organizations to the local chambers of commerce, nonprofit organizations make our communities more livable places. Unlike for-profit businesses that exist to generate profits for their owners, nonprofit organizations exist to pursue missions that address the needs of society. Nonprofit organizations serve in a variety of sectors, such as religious, education, health, social services, commerce, amateur sports clubs, and the arts.

Illustration of the Statement of Financial Position and the Statement of Activities

We are now ready to present examples of the statement of financial position and the statement of activities. To do that, we'll follow the activities of a nonprofit organization called Home4U, a daytime shelter for adults.

Let's assume that Home4U was incorporated in January 2013 and its accounting years will end on each December 31. The following transactions occurred during a three-month period.

Statement of Functional Expenses

The statement of functional expenses is described as a matrix since it reports expenses by their function (programs, management and general, fundraising) and by the nature or type of expense (salaries, rent). For instructional purposes we highlighted the column headings to indicate the expenses by function. We also highlighted the words in the first column as they indicate the nature or type of expenses.

Introduction to Payroll Accounting

It's a fact of business—if a company has employees, it has to account for payroll and fringe benefits.

In this explanation of payroll accounting we'll introduce payroll, fringe benefits, and the payroll-related accounts that a typical company will report on its income statement and balance sheet. Payroll and benefits include items such as:

Salaries, Wages, & Overtime Pay

In this section of payroll accounting we focus on the gross amounts earned by the employees of a company.

Salaries

Salaries are usually associated with "white-collar" workers such as office employees, managers, professionals, and executives. Salaried employees are often paid semi-monthly (e.g., on the 15th and last day of the month) or bi-weekly (e.g., every other Friday) and their salaries are often stated as a gross annual amount, such as "$48,000 per year." The "gross" amount refers to the pay an employee would receive before withholdings are made for such things as taxes, contributions to United Way, and savings plans.

Payroll Withholdings: Taxes & Benefits Paid by Employees

This section of payroll accounting focuses on the amounts withheld from employees' gross pay. (In Part 4 of payroll accounting we will discuss the payroll taxes that are not withheld from employees' gross pay.)

Payroll Taxes, Costs & Benefits Paid by Employers

In addition to salaries and wages, the employer will incur some or all of the following payroll-related expenses:

- Employer portion of Social Security tax

- Employer portion of Medicare tax

- State unemployment tax

- Federal unemployment tax

- Worker compensation insurance

- Employer portion of insurance (health, dental, vision, life, disability)

- Employer paid holidays, vacations, and sick days

- Employer contributions toward 401(k), savings plans, & profit-sharing plans

- Employer contributions to pension plans

- Post-retirement health insurance

Examples of Payroll Journal Entries For Wages

NOTE: In the following examples we assume that the employee's tax rate for Social Security is 6.2% and that the employer's tax rate is 6.2%. (During the years 2011 and 2012 only, the employee's rate was reduced to 4.2%.)

In this section of payroll accounting we will provide examples of the journal entries for recording the gross amount of wages, payroll withholdings, and employer costs related to payroll.

Examples of Payroll Journal Entries For Salaries

Note: In the following examples we assume that the employee's tax rate for Social Security is 6.2% and that the employer's tax rate is 6.2%. (During 2011 and 2012 only, the employee's rate was reduced to 4.2%.)

Let's assume our company also has salaried employees who are paid semimonthly on the 15th and the last day of each month. The pay period for these employees is the half-month that ends on payday. There is one salaried employee in the warehouse department with a gross salary of $48,000 per year, or $2,000 per pay period. There are four salaried employees in the Selling & Administrative Department with combined salaries of $9,000 per pay period.

Introduction to Bookkeeping

The term bookkeeping means different things to different people:

- Some people think that bookkeeping is the same as accounting. They assume that keeping a company's books and preparing its financial statements and tax reports are all part of bookkeeping. Accountants do not share their view.

Accrual Method

There are two main methods of accounting (or bookkeeping):

- Accrual method

- Cash method

The accrual method of accounting is the preferred method because it provides:

Double-Entry, Debits and Credits

Double-Entry

Except for some very small companies, the standard method for recording transactions is double-entry. Double-entry bookkeeping or double-entry accounting means that every transaction will involve at least two accounts. To illustrate, here are a few transactions and the two accounts that will be affected:

General Ledger Accounts

The accounts that are used to sort and store transactions are found in the company's general ledger. The general ledger is often arranged according to the following seven classifications. (A few examples of the related account titles are shown in parentheses.)

Debits and Credits in the Accounts

If you already understand debits and credits, the following table summarizes how debits and credits are used in the accounts.

Asset Accounts

Asset accounts are one of the three major classifications of balance sheet accounts:

- Assets

- Liabilities

- Stockholders' equity (or owner's equity)

Liability and Stockholders' Equity Accounts

Liability Accounts

A company's liability accounts appear in the chart of accounts, general ledger, and balance sheet immediately following the asset accounts. In the general ledger, the liability accounts will usually have credit balances.

Income Statement Accounts

The income statement accounts are categorized in a variety of ways. Here are the classifications we will be using:

- Operating revenues

- Operating expenses

- Other revenues and gains

- Other expenses and losses

Recording Transactions

With sophisticated accounting software and inexpensive computers, it is no longer practical for most businesses to manually enter transactions into journals and then to post to the general ledger accounts and subsidiary ledger accounts. Today, software such as QuickBooks* will update the relevant accounts and provide more information with a minimum of data entry.

Adjusting Entries

Why adjusting entries are needed

In order for a company's financial statements to be complete and to reflect the accrual method of accounting, adjusting entries must be processed before the financial statements are issued. Here are three situations that describe why adjusting entries are needed:

Balance Sheet

The balance sheet is one of the four main financial statements of a business:

- Balance Sheet

- Income Statement

- Cash Flow Statement

- Statement of Stockholders' Equity

Cash Flow Statement

While the balance sheet and the income statement are the most frequently referenced financial statements, thestatement of cash flows or cash flow statement is a very important financial statement.

The cash flow statement is important because the income statement and balance sheet are normally prepared using the accrual method of accounting. Hence the revenues reported on the income statement were earned but the company may not have received the money from its customers. (Many times companies allow customers to pay in 30 days or 60 days and often customers pay later than the agreed upon terms.) Similarly the expenses that are reported on the income statement have occurred, but the company may not have paid for the expense in the same period. In order to understand how cash has changed, and because many believe that "cash is king" the cash flow statement should be distributed and read at the same time as the income statement and balance sheet.

Statement of Stockholders' Equity

The fourth financial statement is the statement of stockholders' equity. This statement lists the changes to the stockholders' equity section of the balance sheet during the current accounting period. A comparative statement of stockholders' equity will also report the amounts for the previous period.

Sample Transactions #4 - #6

Sample Transaction #4

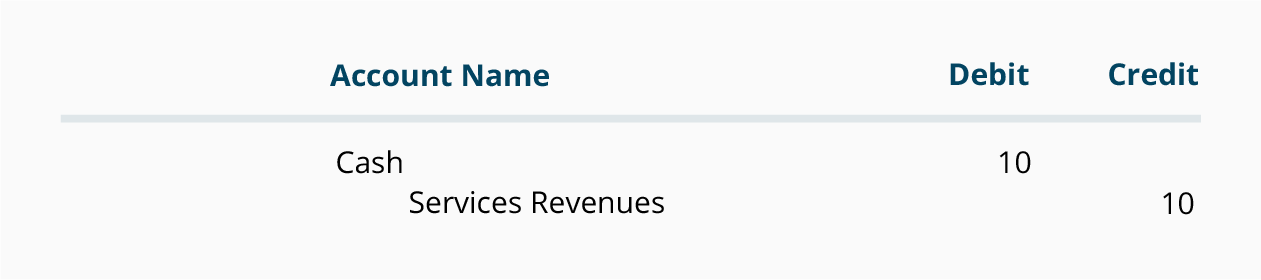

The fourth transaction occurs on December 3, when a customer gives Direct Delivery a check for $10 to deliver two parcels on that day. Because of double entry, we know there must be a minimum of two accounts involved—one of the accounts must be debited, and one of the accounts must be credited.

Because Direct Delivery received $10, it must debit the account Cash. It must also credit a second account for $10. The second account will be Service Revenues, an income statement account. The reason Service Revenues is credited is because Direct Delivery must report that it earned $10 (not because it received $10). Recording revenues when they are earned results from a basic accounting principle known as the revenue recognition principle. The following tip reflects that principle.

Here's a Tip

Revenues accounts are credited when the company earns a fee (or sells merchandise) regardless of whether cash is received at the time.

Here are the two parts of the transaction as they would look in the general journal format:

Sample Transaction #5

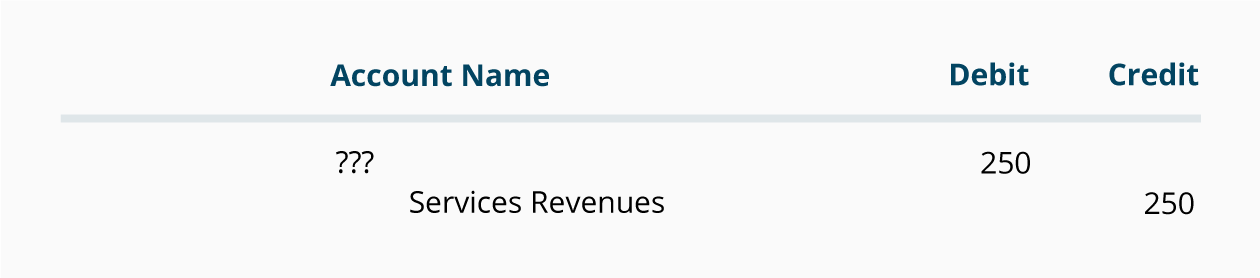

Let's assume that on December 3 the company gets its second customer-a local company that needs to have 50 parcels delivered immediately. Joe's price of $250 is very appealing, so Joe's company is hired to deliver the parcels. The customer tells Joe to submit an invoice for the $250, and they will pay it within seven days.

Joe delivers the 50 parcels on December 3 as agreed, meaning that on December 3 Direct Delivery has earned$250. Hence the $250 is reported as revenues on December 3, even though the company did not receive any cash on that day. The effort needed to complete the job was done on December 3. (Depositing the check for $250 in the bank when it arrives seven days later is not considered to take any effort.)

Let's identify the two accounts involved and determine which needs a debit and which needs a credit.

Because Direct Delivery has earned the fees, one account will be a revenues account, such as Service Revenues. (If you refer back to the last TIP, you will read that revenue accounts—such as Service Revenues—are usually credited, meaning the second account will need to be debited.)

In the general journal format, here's what we have identified so far:

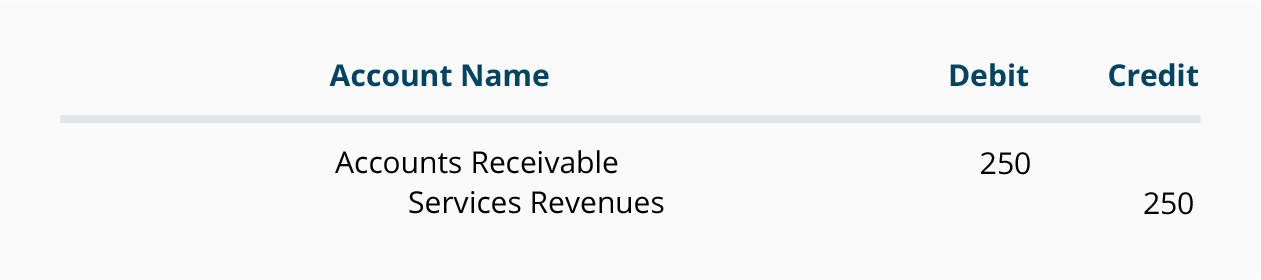

We know that the unnamed account cannot be Cash because the company did not receive money on December 3. However, the company has earned the right to receive the money in seven days. The account title for the money that Direct Delivery has a right to receive for having provided the service is Accounts Receivable (an asset account).

Again, reporting revenues when they are earned results from the basic accounting principle known as the revenue recognition principle.

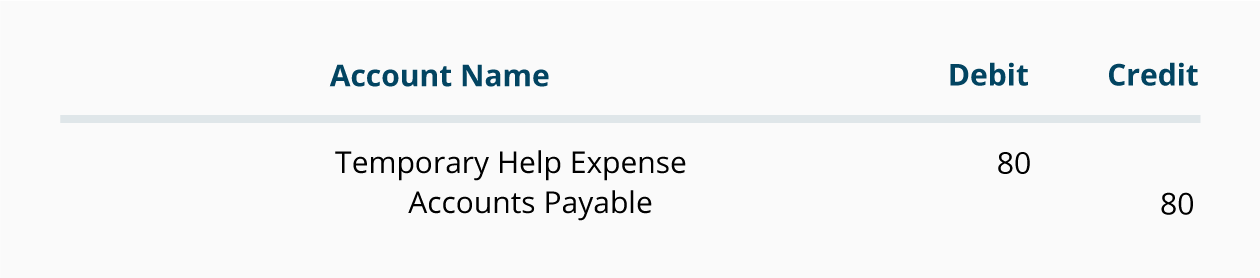

Sample Transaction #6

For simplicity, let's assume that the only expense incurred by Direct Delivery so far was a fee to a temporary help agency for a person to help Joe deliver parcels on December 3. The temp agency fee is $80 and is due by December 12.

If a company does not pay cash immediately, you cannot credit Cash. But because the company owes someone the money for its purchase, we say it has an obligation or liability to pay. Most accounts involved with obligations have the word "payable" in their name, and one of the most frequently used accounts is Accounts Payable. Also keep in mind that expenses are almost always debited.

The accounts and amounts for the temporary help are:

Here's a Tip

Expenses are (almost) always debited.

Here's a Tip

If a company does not pay cash right away for an expense or for an asset, you cannot credit Cash. Because the company owes someone the money for its purchase, we say it has an obligation or liability to pay. The most likely liability account involved in business obligations is Accounts Payable.

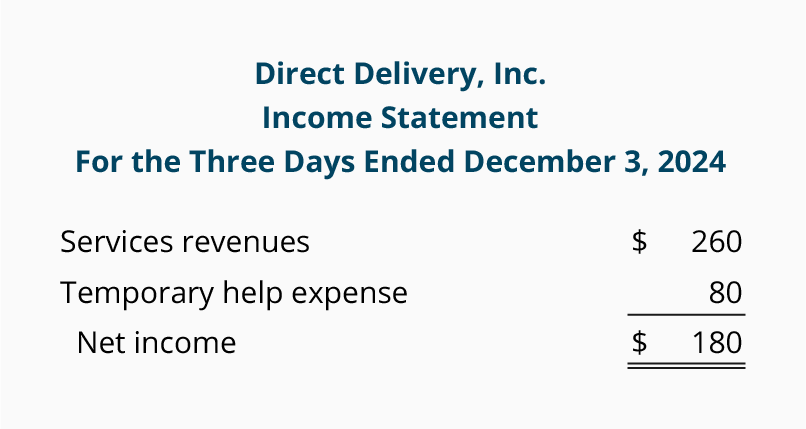

Revenues and expenses appear on the income statement as shown below:

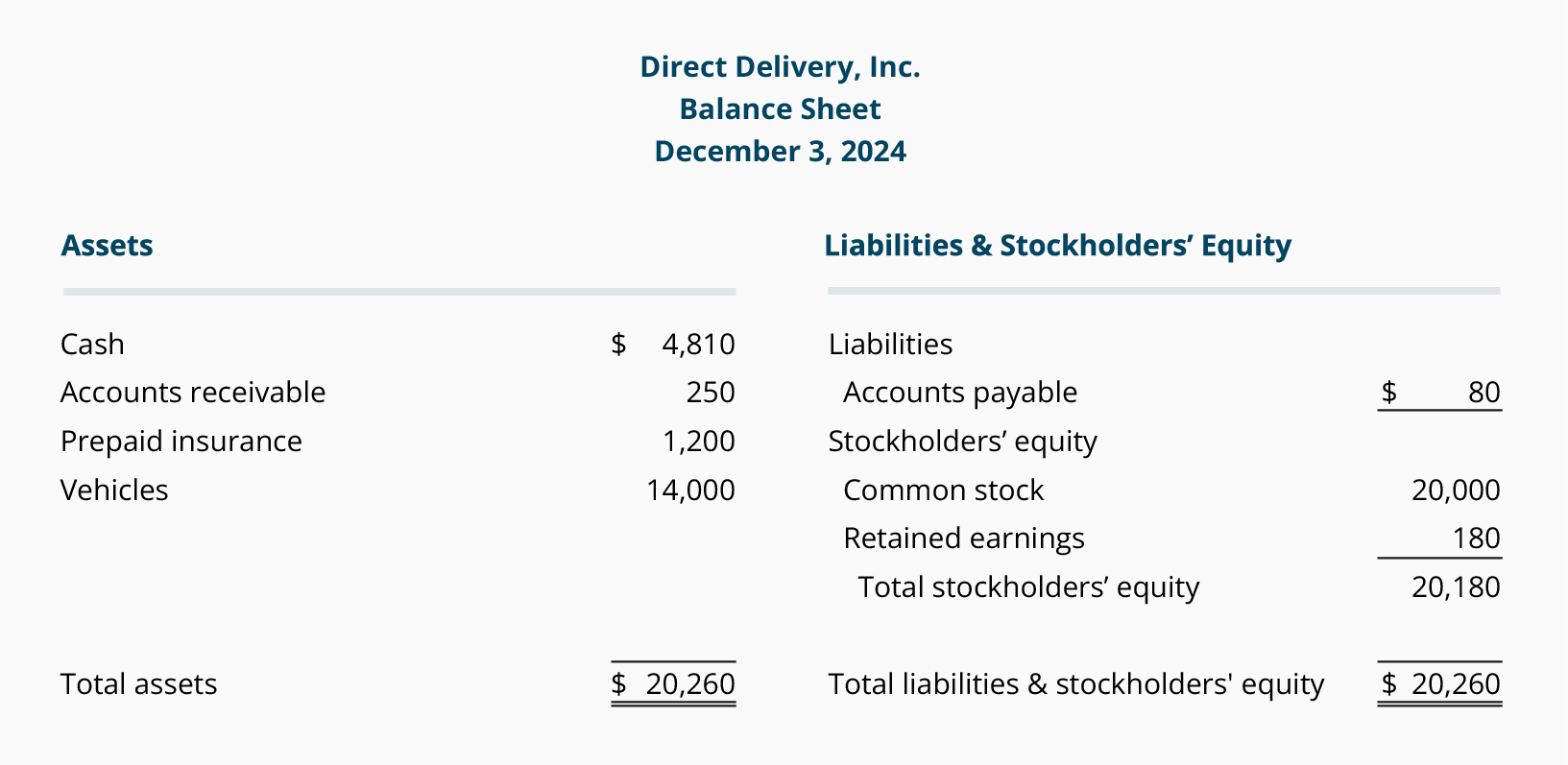

After the entries through December 3 have been recorded, the balance sheet will look like this:

Notice that the year-to-date net income (bottom line of the income statement) increased Stockholders' Equity by the same amount, $180. This connection between the income statement and balance sheet is important. For one, it keeps the balance sheet and the accounting equation in balance. Secondly, it demonstrates that revenues will cause the stockholders' equity to increase and expenses will cause stockholders' equity to decrease. After the end of the year financial statements are prepared, you will see that the income statement accounts (revenue accounts and expense accounts) will be closed or zeroed out and their balances will be transferred into the Retained Earnings account. This will mean the revenue and expense accounts will start the new year with zero balances—allowing the company "to keep score" for the new year.

Marilyn suggested that perhaps this introduction was enough material for their first meeting. She wrote out the following notes, summarizing for Joe the important points of their discussion:

- When a company pays cash for something, the company will credit Cash and will have to debit a second account. Assuming that a company prepares monthly financial statements—

- If the amount is used up or will expire in the current month, the account to be debited will be an expense account. (Advertising Expense, Rent Expense, Wages Expense are three examples.)

- If the amount is not used up or does not expire in the current month, the account to be debited will be an asset account. (Examples are Prepaid Insurance, Supplies, Prepaid Rent, Prepaid Advertising, Prepaid Association Dues, Land, Buildings, and Equipment.)

- If the amount reduces a company's obligations, the account to be debited will be a liability account. (Examples include Accounts Payable, Notes Payable, Wages Payable, and Interest Payable.)

- When a company receives cash, the company will debit Cash and will have to credit another account. Assuming that a company will prepare monthly financial statements—

- If the amount received is from a cash sale, or for a service that has just been performed but has not yet been recorded, the account to be credited is a revenue account such as Service Revenues or Fees Earned.

- If the amount received is an advance payment for a service that has not yet been performed or earned, the account to be credited is Unearned Revenue.

- If the amount received is a payment from a customer for a sale or service delivered earlier and has already been recorded as revenue, the account to be credited is Accounts Receivable.

- If the amount received is the proceeds from the company signing a promissory note, the account to be credited is Notes Payable.

- If the amount received is an investment of additional money by the owner of the corporation, a stockholders' equity account such as Common Stock is credited.

Note: To learn more about debits and credits, go to Explanation of Debits and Credits and Quiz for Debits and Credits. - Revenues are recorded as Service Revenues or Sales when the service or sale has been performed, notwhen the cash is received. This reflects the basic accounting principle known as the revenue recognition principle.

- Expenses are matched with revenues or with the period of time shown in the heading of the income statement, not in the period when the expenses were paid. This reflects the basic accounting principle known as the matching principle.

- The financial statements also reflect the basic accounting principle known as the cost principle. This means assets are shown on the balance sheet at their original cost or less and not at their current value. The income statement expenses also reflect the cost principle. For example, the depreciation expense is based on the original cost of the asset being depreciated and not on the current replacement cost.

Additional Information and Resources

Because the material covered here is considered an introduction to this topic, many complexities have been omitted. You should always consult with an accounting professional for assistance with your own specific circumstances.

Subscribe to:

Posts (Atom)